In exploring consumer behaviour across the MENA region, the gap between brick-and-mortar versus digital shopping exists even in the heaviest sales frequency categories (electronics and apparel). Despite the region’s growing e-commerce outlook (eMarketer predicts annual sales will hit $49bn by 2021), Arab consumers still hold back on digital shopping due to a variety of barriers, sceptical notions and incorrect perceptions.

In exploring consumer behaviour across the MENA region, the gap between brick-and-mortar versus digital shopping exists even in the heaviest sales frequency categories (electronics and apparel). Despite the region’s growing e-commerce outlook (eMarketer predicts annual sales will hit $49bn by 2021), Arab consumers still hold back on digital shopping due to a variety of barriers, sceptical notions and incorrect perceptions.

What is stopping them?

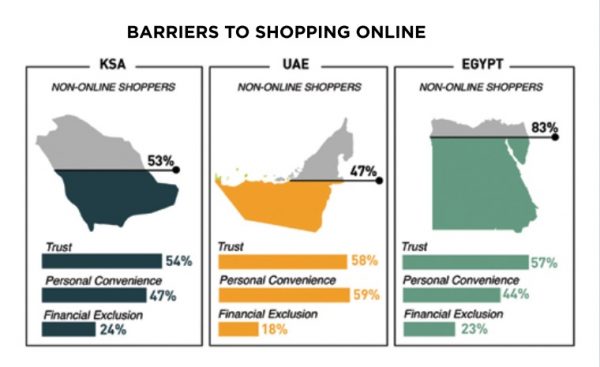

Earlier this year, Choueiri Group conducted some very revealing research. Being ‘unbanked’ or financially excluded (consumers assume they cannot shop online without a credit card or bank account) stood out prominently. Despite most e-commerce platforms offering shoppers cash-on-delivery (COD), two out of 10 Egyptians and 18 per cent of the Saudi sample did not shop online due to financial exclusion. 11 per cent in KSA said they preferred to pay in cash so did not pursue digital

shopping. Cash is still the prevalent purchasing method in the region, even across more economically developed markets, and the Saudi Communication and Information Technology Commission states that 66 per cent of shoppers use COD to make digital purchases, making it the second most popular

payment method after credit cards (87 per cent). We can conclude there are awareness and educational issues that must be addressed.

Trust was the greatest barrier in various guises. In KSA, the inability to touch and inspect an item first-hand created an obstacle for more than a quarter of consumers. A similar proportion distrusted online shopping in general. Concerns about accidentally buying fake items were raised by 15 per cent, while the questionable quality of online products was cited by 12 per cent. Other barriers included

worrying about personal information, and products not looking as advertised. Even in the UAE, where digital shopping penetration is healthier than in KSA and Egypt, trust came up with nearly three out of 10 respondents.

Many Arab consumers (the non-digital shopper segment) are still driven by the traditional retail experience. In the UAE, shoppers preferred the ‘convenience’ of visiting a real store, trying out the product, interacting with sales staff and instant retrieval of the product. This held especially true when high-value, premium items were concerned.

How is convenience driving growth?

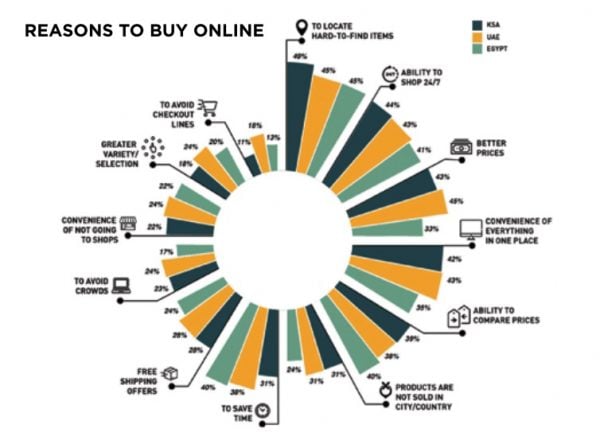

While regional online shopping penetration is in its infancy, or pre-mature stages, depending on the country, many shoppers are moving away from traditional shopping. Just under half of online shoppers said they were motivated by e-commerce platforms and their ability to source hard-to-find items. On average, 27 per cent were triggered to buy online, in order to get products that were only available outside their place of residence.

The future of e-commerce in MENA relies heavily on purposeful communications to catalyse non-digital-shoppers

The future of e-commerce in MENA relies heavily on purposeful communications to catalyse non-digital-shoppers

Prevailing knowledge gaps need to be bridged and the value addition and clear benefits of online shopping need to be communicated to sceptical audiences. Numerous faulty

perceptions deeply associated with digital shopping also need to be addressed. In doing so, brands will help erase the invisible barriers around trust, convenience and the need to have a bank account. With e-commerce players employing many innovative solutions to make online shopping more seamless, further efforts are needed by their media partners and communication experts to change the game.

We recommend educational content and even a ‘back-to-basics’ approach to fill in any necessary knowledge gaps. Combining this approach with uplifting content aimed at capturing audiences on an emotional level will also support behavioural changes.